It certainly had nothing to do with our two-party structure, which was the gist of your reply above.

Of course I’ve wondered. The answers appear to be excessive private debt, encouraged by the Fed as harmless; low taxes, encouraging massive disinvestment and a search for paper wealth; and deregulation, which allowed private speculation to run rampant. Mix in a healthy dose of fraud, and you have a toxic brew.

Quote: “CRA regulations are at the core of Fannie’s and Freddie’s so-called affordable housing mission. In the early 1990s, a Democrat Congress gave HUD the authority to set and enforce (through fines) CRA-grade loan quotas at Fannie and Freddie… It passed a law requiring the government-backed agencies to “assist insured depository institutions to meet their obligations under the (CRA).” The goal was to help banks meet lending quotas by buying their CRA loans.

But they had to loosen underwriting standards to do it. And that’s what they did.”

CRA accounted for no more than a smattering of the loans, most of which, according to the FBI, involved fraud in the inducement. In addition, Fanny and Freddie did not join the party until it was well underway, as they had to keep market share.

You have no sense of proportion, and no ability other than to self-validated by seeking evidence that confirms your bias to the exclusion of all else. I could go get some numbers, but not for you. I could suggest you read some books, but you won’t. Forget it. OK?

Simple economics Mark. Force lending institutions to loan with 3% down to people with questionable credit and no jobs and you get a massive housing boom. Inventories shrink, prices rise until of course it all comes crashing down.

Sinn Fein was a sine wave.

LikeLike

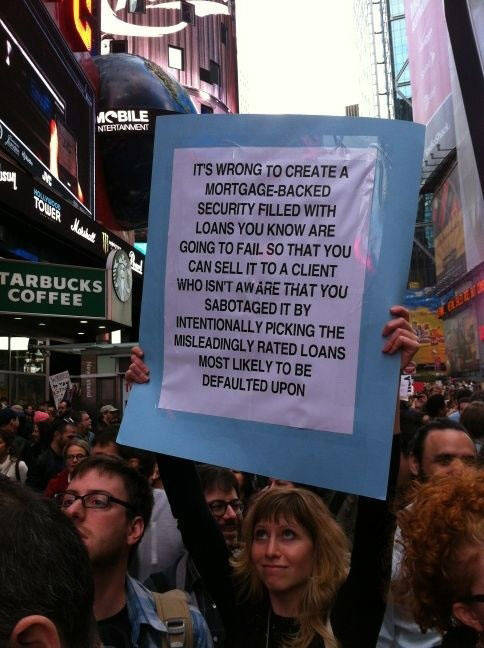

Didn’t get past the first sign.

Ya know, the one about the banks and their sabotage.

http://directorblue.blogspot.com/2013/02/nber-yep-bill-clinton-andrew-cuomo-and.html

LikeLike

Can’t shake that old party thinking. They got you young, right? Old dog, no new tricks.

LikeLike

You’re the older dog here Mark.

Did it ever make you wonder just why we had these massive defaults in the first place?

When for the previous 50 years the percentage was much smaller.

LikeLike

It certainly had nothing to do with our two-party structure, which was the gist of your reply above.

Of course I’ve wondered. The answers appear to be excessive private debt, encouraged by the Fed as harmless; low taxes, encouraging massive disinvestment and a search for paper wealth; and deregulation, which allowed private speculation to run rampant. Mix in a healthy dose of fraud, and you have a toxic brew.

LikeLike

Bullsh*t.

Quote: “CRA regulations are at the core of Fannie’s and Freddie’s so-called affordable housing mission. In the early 1990s, a Democrat Congress gave HUD the authority to set and enforce (through fines) CRA-grade loan quotas at Fannie and Freddie… It passed a law requiring the government-backed agencies to “assist insured depository institutions to meet their obligations under the (CRA).” The goal was to help banks meet lending quotas by buying their CRA loans.

But they had to loosen underwriting standards to do it. And that’s what they did.”

CRA=Community Reinvestment Act.

LikeLike

CRA accounted for no more than a smattering of the loans, most of which, according to the FBI, involved fraud in the inducement. In addition, Fanny and Freddie did not join the party until it was well underway, as they had to keep market share.

LikeLike

Really. How about 6.1 trillion in CRA loans in 2000 Mark? Rising from less than a 100B when the rules were tighten in 1995.

Defaults rates around 20%. You do the math.

LikeLike

You have no sense of proportion, and no ability other than to self-validated by seeking evidence that confirms your bias to the exclusion of all else. I could go get some numbers, but not for you. I could suggest you read some books, but you won’t. Forget it. OK?

LikeLike

I take that as a win.

Simple economics Mark. Force lending institutions to loan with 3% down to people with questionable credit and no jobs and you get a massive housing boom. Inventories shrink, prices rise until of course it all comes crashing down.

Simpletons blame banks.

LikeLike

The FBI is then comprised of simpletons?

LikeLike